Investor DSCR Mortgage Loans – No Income Required

What Is the Debt Service Coverage Ratio (DSCR)?

The debt service coverage ratio is a ratio of a property’s annual gross rental income and its annual mortgage debt, including principal, interest, taxes, insurance, and HOA (if applicable). Lenders use DSCR to analyze how much of a loan can be supported by the income coming from the property as well as to determine how much income coverage there will be at a specific loan amount. Lenders do not take into account expenses such as management, maintenance, utilities, vacancy rate, or repairs in the debt-service-coverage ratio calculation.

What Is a DSCR Loan?

A DSCR loan is a type of Non-QM loan for real estate investors. Lenders use a DSCR to help qualify real estate investors for a loan because it can easily determine the borrower’s ability to repay without verifying income.

A DSCR loan is one of several types of home loans referred to as Non-QM loans. Non-QM loans provide potential borrowers with an alternative route to financing, which doesn’t require traditional income verification methods.

A DSCR loan in particular makes it easier to show rental income that might not show up on your taxes due to deductions for legitimate business expenses.

A DSCR loan enables real estate investors to get a loan because it takes into account cash flow from investment properties rather than pay stubs or W-2s, which many investors do not typically have. Lenders use DSCR to evaluate a borrower’s ability to make monthly loan payments.

Deductions from properties may lower taxable income, making it hard for investors to prove their true income. Lenders use DSCR to determine whether someone can make loan repayments. Otherwise, many investors might struggle to meet the basic eligibility standards for real estate loans.

Since they don’t require pay stubs or tax returns showing minimum income levels, debt service coverage ratio loans are a great alternative for investors who claim many write-offs and business deductions.

What Matters in a DSCR Loan?

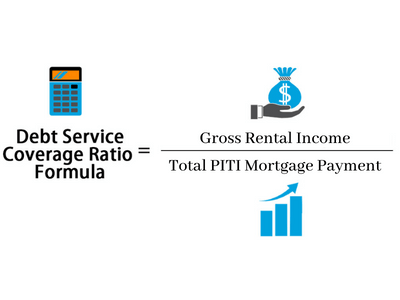

The debt service coverage ratio formula is the annual gross rental income divided by the debt obligations of the property.

- To find your gross rental income, we take your annual rental income based on your lease agreement and the appraiser’s comparable rent schedule (form 1007) and use the lesser of the two. In some cases, if you can prove a twelve-month history of LTR or STR rental income, you can qualify off that rather than the appraiser’s market rent.

- Next, you’ll need to find your annual debt. Your annual debt for loan qualification purposes equals the total annual principal, interest, taxes, insurance, and HOA (if applicable) payments. Annual Debt = Total Annual PITI payments.

- Next, you’ll divide your annual gross rental income by your annual debt for your ratio. DSCR = Annual gross rental income/Annual Debt.

Please note that net operating income (NOI), capitalization rate (Cap Rate), cash on cash return (COCR), and return on investment (ROI) are not considered for DSCR mortgage loan qualifying purposes.

Example of Debt Service Coverage Ratio Calculation

A real estate investor might be looking at a property with a gross rental income of $50,000 and an annual debt of $40,000. When you divide $50,000 by $40,000, you get a DSCR of 1.25, which means that the property generates 25% more income than what is necessary to repay the loan. This also means that there is a positive cash flow in the lender’s eye.

Why Does DSCR Matter?

The debt service coverage ratio lets the lender know how to determine a borrower’s ability to pay off their DSCR mortgage. Lenders must forecast how much a real estate property can rent for so that they can predict a property’s rental value.If you have a DSCR of less than 1.0, it means that a property has the potential for negative cash flow. DSCR loans can still be made on properties with less than a 1 ratio however they usually are purchase loans with home improvements, upgrades, or remodeling to be made to increase the monthly rent or for homes with high equity and potential for higher rents in the future. You also can potentially get the property above a 1.0 ratio with a DSCR interest-only loan.

Non-QM Loans for Borrowers with Low DSCR

- Asset-Based Loans: Asset-based mortgages are another loan product for investors who want to qualify for a loan without taking income into account. These loans allow you to use your assets instead of your income to qualify, which means you won’t have to provide a tax return or proof of income..

- Bank Statement Loans: A bank statement loan allows investors to verify their income using bank statements instead of tax returns. These are beneficial for investors who have write-offs and deductions on their taxes that may make lenders believe that they bring in less money than they actually do each month.

- Interest-Only Loans: Interest-only loans offer investors the option to pay lower monthly payments for the first portion of the loan. During this time, payments only apply to interest, not the principal balance.

- Recent Credit Event Loans: A recent credit event loan allows borrowers to qualify for a loan despite recent credit events like bankruptcy, short sale, foreclosure, and divorce so that you can start rebuilding your investment portfolio as soon as possible.

- Near Miss Jumbo Loans: Near miss jumbo loans offer flexible qualification requirements and allow individuals to borrow large sums with as little as 10% down.